Why Segregation of Duties Is Critical to Fraud Prevention

One of the most effective ways to reduce fraud risk within an organization is through proper segregation of duties. Fraud often occurs when a single individual has excessive control over a process, allowing them to initiate, approve, record, and conceal transactions without oversight. By separating key responsibilities among multiple employees, organizations create a system of checks and balances that significantly reduces opportunities for misconduct.

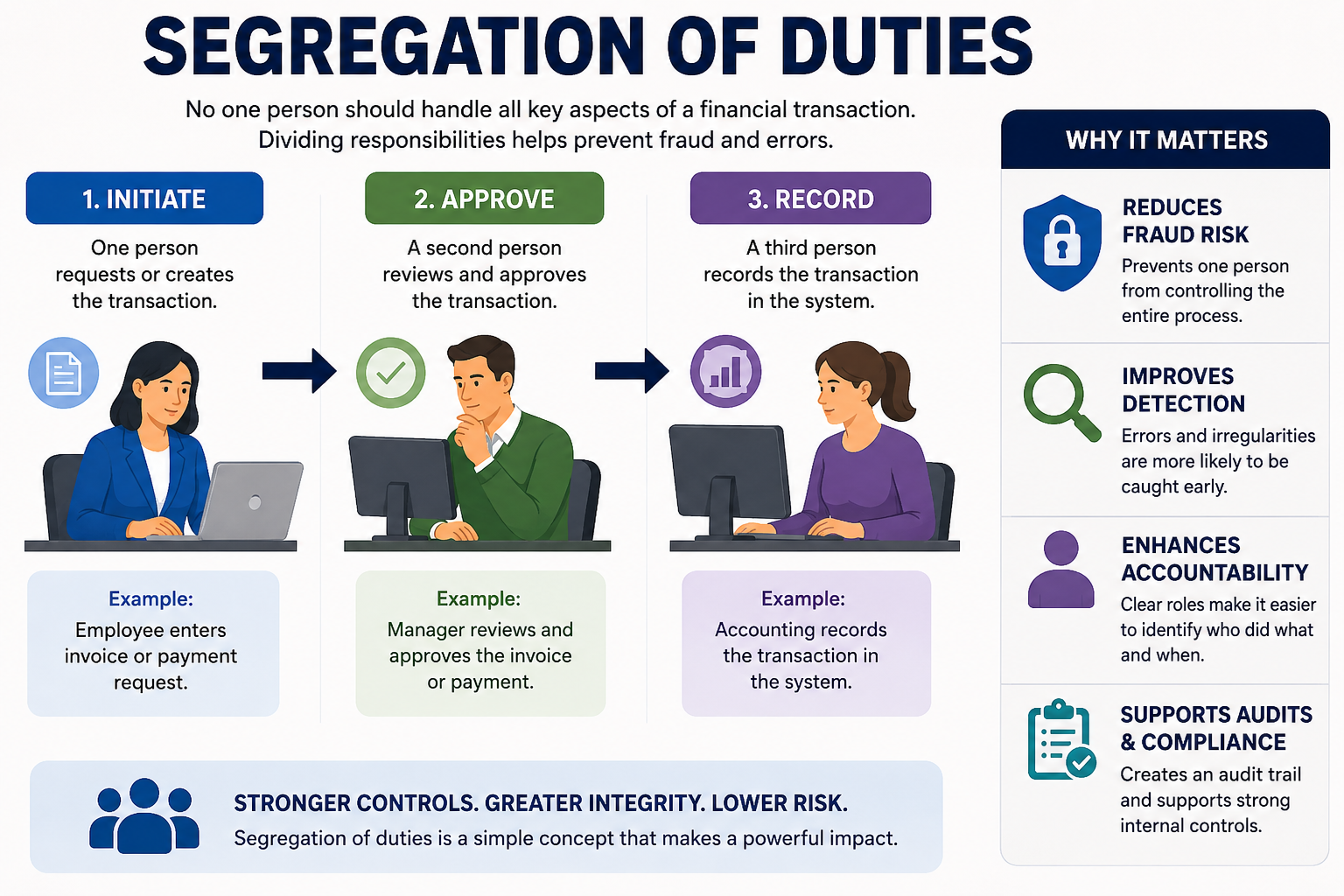

At its foundation, segregation of duties ensures that no one person has complete control over a financial transaction from beginning to end. For example, one employee may initiate a payment request, another may approve it, and a third may record the transaction in the accounting system. This division of responsibilities helps prevent unauthorized activity while increasing the likelihood that errors or irregularities will be detected promptly.

Reducing Opportunities for Fraud

Fraud typically requires three elements: pressure, rationalization, and opportunity. While organizations may have limited ability to control personal pressures or rationalizations, they can directly reduce opportunities through strong internal controls.

When a single employee has the ability to create vendors, approve invoices, and issue payments, the potential exists for fictitious vendors, unauthorized disbursements, or concealed transactions. Segregation of duties disrupts this risk by requiring multiple individuals to participate in critical processes, making fraudulent schemes more difficult to execute and easier to uncover.

This control is particularly important in high-risk areas such as:

- Accounts payable

- Payroll processing

- Procurement and purchasing

- Expense reimbursements

- Cash management

- Journal entry preparation and approval

By separating responsibilities within these functions, organizations establish safeguards that protect assets and strengthen financial integrity.

Strengthening Accountability and Transparency

Beyond fraud prevention, segregation of duties enhances accountability throughout the organization. Clearly defined roles make it easier to identify who performed specific tasks, approved transactions, and reviewed supporting documentation.

This transparency benefits management, auditors, and stakeholders by providing a clear audit trail and facilitating more efficient investigations when issues arise. Employees are also more likely to follow established procedures when they know their work will be independently reviewed by others.

Effective internal controls are not based solely on trust. Rather, they are designed to verify that processes are operating as intended and that transactions are properly authorized and documented.

Common Challenges Organizations Face

Many organizations mistakenly believe that segregation of duties is only necessary for large corporations. In reality, small and mid-sized businesses often face greater risks because limited staffing requires employees to perform multiple functions.

As organizations grow, internal controls must evolve as well. Processes that were appropriate when a company had a handful of employees may become inadequate as operations expand. Management should periodically review job responsibilities, approval authorities, and system access rights to ensure duties remain appropriately segregated.

Another common weakness is excessive reliance on supervisory review. While management oversight is important, it should not replace properly designed controls. If a single manager can authorize, process, review, and reconcile transactions without independent oversight, significant risk remains.

Practical Applications

Implementing segregation of duties does not require a complex organizational structure. Companies can begin by mapping critical business processes and identifying who is responsible for initiating, approving, recording, and reviewing transactions.

Examples of effective segregation include:

- One employee enters invoices while another approves payment.

- One employee processes payroll while another reviews and releases payroll transactions.

- One employee creates vendor records while another approves new vendors.

- One employee performs bank reconciliations but does not have authority to issue payments.

- One employee prepares journal entries while another reviews and approves them.

Technology can further strengthen these controls through user-access restrictions, automated approval workflows, exception reporting, and audit logs. However, technology should support—not replace—management oversight and periodic review.

The Bottom Line

Segregation of duties remains one of the most powerful internal controls available to organizations. By dividing responsibilities, companies reduce opportunities for fraud, improve accountability, and increase the likelihood that errors or irregularities will be identified before they result in financial loss.

Fraud often hides within routine business activities. Strong segregation of duties helps ensure that no single individual has the ability to manipulate a process without detection. Organizations that prioritize this control demonstrate a commitment to sound governance, financial integrity, and responsible stewardship of company resources.

Trust is important in every organization, but effective internal controls recognize that verification is equally essential. Maintaining the proper balance between the two is a key component of a successful fraud prevention strategy.

This version is written in a more professional tone and aligns well with forensic accounting, internal audit, and fraud-risk-management audiences.